TRG | The Bottom Line – 7/14

As we hit the midway point of the year, we believe it is helpful to compare where we are now vs. where industry participants in the resi market thought we would be. The key point – first half results, though down meaningfully overall, have been markedly better than companies’ budgeted. Many companies have much easier comps in the second half, and therefore expect YOY declines to be much more modest than 1H. All of this is happening in the face of a banking crisis and mortgage rates drifting upward to near 7%, which is remarkable in our view.

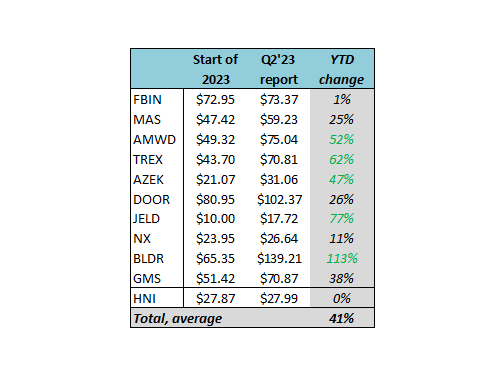

So what about the stocks? As we pointed out in our Q2’23 Residential Products Survey, the stocks in the group are up ~40% YTD vs. the S&P 500 up 18%. The standout stronger performing stocks have the commonality of entering the year with the lowest expectations (big ticket R&R and highest SF exposure) have been best performers – AMWD up 52%, TREX up 62%, AZEK up 47%, BLDR up 113%, GMS up 38%, and JELD up 77% (JELD more of an isolated case for low expectations).

What from here? Be more selective vs. broadly contrarian. The 12-month outlook drove stock prices in the group down in throughout 2022. This started to reverse in late 2022 to current. We think the go-forward trend remains your friend, but with stock prices up, investors must be selective on stories and exposures. We plan to highlight ideas that fit this criteria in an upcoming note.